Cracks in the Super-Long End: Japan’s 20-Year Auction Demand Hits 9-Month Low

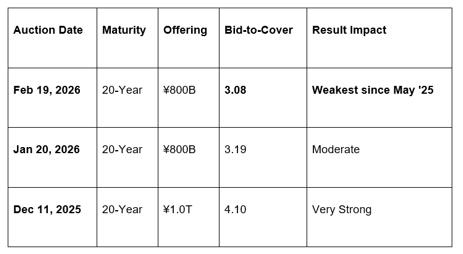

In a signal that investors are becoming increasingly wary of Japan’s shifting fiscal landscape, the Ministry of Finance's February 19, 2026, auction of 20-year Japanese Government Bonds (JGBs) saw its weakest demand since May 2025.

The bid-to-cover ratio—a key metric of auction health—fell to 3.08, down from 3.19 in the previous sale. While not a catastrophic "failed" auction, the results highlight a growing "fiscal premium" that investors are demanding to hold Japan’s long-dated debt amid Prime Minister Sanae Takaichi’s aggressive reflationary agenda.

1. The Bid-to-Cover Slide: A 9-Month Low

A bid-to-cover ratio of 3.08 means that for every bond the government offered, there were just over three bids. While this remains above the "danger zone" (typically below 2.0), the downward trend is alarming to market participants.

May 2025 Echoes: The last time demand was this soft was in May 2025, a period defined by extreme volatility following the announcement of U.S. "Liberation Day" tariffs.

The "Tail" Concern: Market reports suggest the "tail"—the gap between the average and lowest accepted price—widened, indicating that the Ministry had to accept significantly lower prices (higher yields) to clear the ¥800 billion offering.

Lack of "Lifers": Traditional buyers of 20-year debt, such as Japanese life insurance companies, appear to be sitting on the sidelines. With yields rising beyond their year-end projections, many are reluctant to buy now and risk further "unrealized losses" on their balance sheets.

2. Why is Demand Softening?

The "Takaichi Factor" is the primary driver of this auction's lackluster performance. Following her landslide election victory on February 8, the market is bracing for a "Two-Year Overhaul" of the national budget.

Tax Cut Uncertainty: Takaichi’s plan to suspend the 8% consumption tax on food creates a ¥5 trillion annual revenue hole. Investors are skeptical that "structural savings" can fill this gap without new deficit-financing bonds.

Monetary Policy Lag: Despite inflation holding near 3%, the Bank of Japan (BoJ) has remained relatively cautious. Bondholders fear that if the BoJ stays behind the curve to support Takaichi's growth plans, long-term inflation will erode the value of 20-year fixed payments.

The AI Infrastructure Buildout: The government's pledge of over ¥10 trillion for semiconductors and AI further complicates the long-term debt trajectory, leading investors to demand a "higher yield for higher risk."

3. Market Reaction: Yield Curve Steepening

The immediate aftermath of the auction saw the 20-year JGB yield tick higher, contributing to a "bear steepening" of the Japanese yield curve.

The 10Y-20Y Spread: The spread between the 10-year and 20-year yields has widened as the market prices in greater uncertainty for "super-long" durations.

Secondary Market Sell-off: JGB futures softened as dealers who took down the auction "inventory" immediately looked to hedge their positions, further weighing on prices.

GME Academy Analysis: "The JGB Trap"

At Global Markets Eruditio, we are advising clients to watch the ¥1.2 trillion 30-year auction scheduled for early March.

Trader's Takeaway for February 2026:

JGB Short Bias: As long as the funding for Takaichi’s "Food Tax Cut" remains vague, the path of least resistance for long-end yields is up. We are targeting a 2.65% yield on the 20-year by the end of Q1.

Yen Correlation: Usually, higher yields support the currency. However, if yields are rising due to "fiscal fear" rather than "growth," the Yen (JPY) may actually weaken. Watch the USD/JPY 158.00 level closely.

Institutional Shift: If domestic "Lifers" don't return to the market in March, the BoJ may be forced to intervene with an unscheduled bond-buying operation (Rinban), which would paradoxically weaken the Yen further.

Join our FREE Macro Workshop at Global Markets Eruditio!

Is Japan facing a "Fiscal Cliff" in 2026? We’ll break down the Ministry of Finance's Q2 Issuance Calendar and show you how to trade the JGB/UST spread.