UK Industry’s Bittersweet 2025: Annual Growth Returns Despite December Chill

The UK’s production sector closed 2025 on a historic, albeit shaky, note. According to the latest Index of Production data released by the Office for National Statistics (ONS) on February 12, 2026, the United Kingdom recorded its first annual increase in production output since 2021.

However, the "December Chill" was real: while the fourth quarter showed resilience, a sharp monthly drop in December reminded traders that the road to industrial recovery remains paved with volatility. At the GME Academy, we call this a "Dead Cat Bounce" warning—annual growth is back, but the monthly momentum is flagging.

1. The Big Picture: A Year of Slow Gains

For the first time in four years, the UK production sector stayed in the green for the full year.

Annual Growth: Production output rose 0.2% in 2025. While modest, it breaks a three-year streak of annual declines.

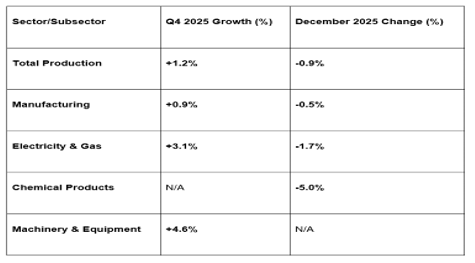

Quarterly Strength (Q4): The three months from October to December saw a robust 1.2% increase compared to Q3.

The Drivers: This quarterly boost was fueled by a 3.1% jump in electricity and gas supply and a 0.9% rise in manufacturing.

2. The December Slump: Widespread Weakness

Despite the strong quarterly average, December was a "month to forget" for UK factories and energy providers.

● Monthly Drop: Output fell by 0.9% in December alone, erasing some of the gains from a strong October and November.

● Sector-Wide Decline: All four main sectors of production contracted in December:

Water & Waste: -2.4%

Electricity & Gas: -1.7%

Mining & Quarrying: -0.7%

Manufacturing: -0.5%

● Manufacturing Specifics: The biggest drags came from Chemical Products (-5.0%), Basic Pharmaceuticals (-2.6%), and Food Products (-1.4%).

3. Manufacturing’s "Two-Speed" Recovery

Within the manufacturing sector, the story of 2025 was one of high-tech winners and traditional losers.

The High-Tech Surge: Subsectors like "Other Manufacturing" (+5.3%) and "Machinery and Equipment" (+4.6%) were the stars of Q4, likely driven by the ongoing AI hardware buildout and aerospace demand.

The Defensive Lag: Basic essentials like food and chemicals struggled as high energy costs and shifting trade patterns late in the year took their toll.

The GME Academy Analysis: "Sterling’s Industrial Anchor"

At Global Markets Eruditio, we look at these numbers to determine the strength of the British Pound (GBP) against its peers.

Trader's Takeaway for February 2026:

GBP/USD Neutral: The annual growth of 0.2% provides a "floor" for the Pound, but the December slump suggests the Bank of England (BoE) may have to remain cautious about future rate hikes if the industrial base is weakening.

Sector Divergence: If you are trading UK equities, the strength in Machinery and Electronics suggests that high-value engineering firms are the place to be, whereas the Chemicals and Pharma sectors face immediate headwinds.

The "Budget Hangover": Much of the December weakness is attributed to business uncertainty following the late Autumn Budget. As clarity returns in Q1 2026, we expect a modest rebound in manufacturing orders.

Join our FREE Forex Workshop at Global Markets Eruditio!

Do you know how to trade "Economic Divergence"? We’ll show you why the UK is growing while other European neighbors are stalling, and how to position your GBP/EUR trades for the spring of 2026.