PBoC Slashes FX Risk Reserves: China Moves to Curb Yuan Strength and Boost Liquidity

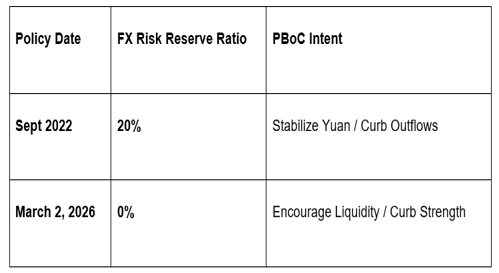

In a significant policy shift aimed at easing the upward pressure on the Renminbi, the People’s Bank of China (PBoC) announced on Friday, February 27, 2026, that it will eliminate the foreign exchange risk reserve ratio for forward sales. Starting March 2, 2026, the ratio will be lowered from 20% to 0%.

The move is seen as a clear signal from Beijing that it is comfortable with a more flexible—and potentially weaker—Yuan as it seeks to support its export sector amid shifting global trade dynamics.

1. What is the FX Risk Reserve Ratio?

The FX risk reserve ratio is a macroprudential tool used by the PBoC to manage currency volatility. When the ratio is set at 20%, financial institutions are required to set aside 20% of the previous month's forward FX sales as reserves at the central bank, with zero interest.

The Mechanism: By making it more expensive for banks and clients to buy Dollars (shorting the Yuan) via forward contracts, the PBoC effectively slows down capital outflows.

The Shift to 0%: Lowering the ratio to zero removes this "tax" on forward dollar purchases. This makes it cheaper for businesses and investors to hedge against Yuan depreciation or to move into foreign currencies.

2. Why Now? Countering "Excessive" Yuan Strength

The decision comes as the Yuan has shown surprising resilience against the Greenback and other major peers in early 2026.

Export Competitiveness: With global trade tensions remaining high and tariffs becoming a permanent fixture of the economic landscape, a strong Yuan hurts the competitiveness of Chinese "Made-in-China" goods.

Capital Market Liberalization: Moving the ratio to 0% aligns with Beijing's longer-term goal of allowing market forces to play a larger role in determining the exchange rate, reducing the need for direct intervention.

Monetary Policy Divergence: As the PBoC maintains a relatively accommodative stance compared to other major central banks, this move provides a "relief valve" for the currency, allowing it to adjust naturally to interest rate differentials.

3. Market Implications: Liquidity and Sentiment

The immediate impact of the announcement was felt across Asian trading desks, as the Yuan softened slightly in the offshore market (CNH).

Increased Forward Trading: Analysts expect a surge in forward FX trading volume starting March 2, as the cost of hedging drops significantly for Chinese importers and multinational corporations.

Sovereign Bond Yields: A more flexible currency policy often allows the central bank more room to maneuver with domestic interest rates. If the Yuan is allowed to weaken, the PBoC may feel more comfortable lowering domestic rates further to stimulate growth.

GME Academy Analysis: "The Yuan’s Controlled Descent"

At Global Markets Eruditio, we interpret this as a tactical move to "prime the pump" for the second quarter of 2026.

Trader's Takeaway for February 2026:

USD/CNY Outlook: The removal of the 20% "penalty" on dollar longs suggests the PBoC is prepared for a move toward the 7.30 - 7.35 level in USD/CNY. Traders should watch for a potential breakout once the 0% ratio takes effect on Monday.

Impact on Commodities: A weaker Yuan typically makes dollar-denominated commodities (like Copper and Iron Ore) more expensive for Chinese buyers. We may see a temporary cooling in commodity demand as the market adjusts to the new FX regime.

Aussie Dollar (AUD) Crosses: As the "liquid proxy" for Chinese growth, the AUD/JPY and AUD/USD pairs may see increased volatility. If the Yuan's move is viewed as a sign of economic managed-softness, the AUD could face short-term headwinds.

Join our FREE Macro Workshop at Global Markets Eruditio!

Is the Yuan ready to tumble? We’ll break down the PBoC Macroprudential Toolkit and show you how to trade the USD/CNH as China pivots its currency policy.