Australian Inflation Sticks at 3.8%: Electricity Surge Offsets Cooling Services

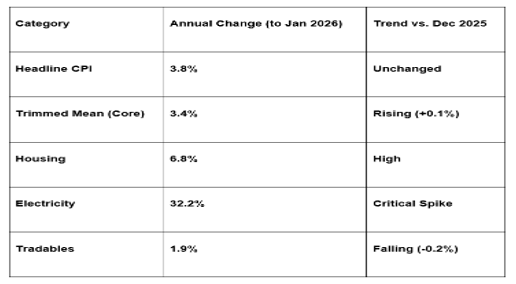

The Reserve Bank of Australia’s (RBA) battle against rising prices hit a stubborn patch in early 2026. According to the latest Consumer Price Index (CPI) data released on Wednesday, February 25, 2026, annual inflation held steady at 3.8% for the 12 months to January, matching the December 2025 figure.

While the headline rate remained unchanged, the underlying data suggests that domestic price pressures are far from extinguished. The Trimmed Mean inflation—the RBA’s preferred measure that filters out extreme price swings—actually ticked upward to 3.4%, signaling that broad-based price increases are becoming more entrenched in the Australian economy.

1. The Domestic Driver: Non-Tradables and Housing

The report highlights a growing divide between goods influenced by global markets and those driven by domestic factors, known as "Non-tradables."

Non-Tradables Surge: Inflation for domestic services and housing rose to 4.9%, up from 4.6% in December. This was fueled by a massive 32.2% spike in Electricity prices over the past year.

Housing Crisis Continues: Housing remains the single largest contributor to inflation, rising 6.8% annually. This includes a 3.9% increase in Rents and a 3.5% rise in the cost of New Dwellings.

Tradables Cooling: In contrast, goods exposed to international trade (Tradables) saw inflation ease to 1.9%, down from 2.1%. While tech gadgets and accessories saw double-digit jumps, the overall trend for imported goods is helping to keep the headline figure from spiraling.

2. Goods vs. Services: A Reversal of Fortune

For much of 2025, services were the primary concern for policymakers. In January 2026, the trend shifted slightly, creating a new set of headaches for the RBA.

Goods Inflation Rebounding: Annual goods inflation jumped to 3.8% (from 3.4% in December). The primary culprit was the energy sector, specifically the aforementioned surge in electricity costs which has permeated the supply chain.

Services Inflation Softening: Services inflation slowed to 3.9% (down from 4.1%). While Medical and Hospital services (+4.2%) and Rents (+3.9%) remain high, the slight cooling in overall services offers a glimmer of hope for a "soft landing" if energy costs can be contained.

3. Monthly Momentum and RBA Outlook

In the month of January alone, the CPI rose 0.5% in seasonally adjusted terms. This monthly momentum suggests that inflation is currently running at an annualized rate that exceeds the RBA's 2–3% target range.

The "sticky" nature of the Trimmed Mean suggests that core inflation is not retreating as fast as the headline figures might imply. This puts the RBA in a difficult position: keeping rates high enough to dampen domestic demand without crushing a housing market already under significant stress.

GME Academy Analysis: "The Hawkish Hold"

At Global Markets Eruditio, we are analyzing this data as a "Hawkish Hold" for the Australian Dollar (AUD).

Trader's Takeaway for February 2026:

AUD/USD Impact: The rise in Trimmed Mean inflation (3.4%) makes it highly unlikely that the RBA will consider interest rate cuts in the first half of 2026. This "sticky" inflation supports the AUD against currencies like the USD or NZD if their respective central banks shift toward a more dovish stance.

Energy Stocks vs. Consumer Discretionary: The 32.2% jump in electricity prices is a massive headwind for household budgets. We are leaning Underweight Consumer Discretionary (retail/dining) as Australians divert more income to utility bills.

The "Non-Tradable" Trap: As long as domestic inflation (4.9%) remains high, the RBA must keep the "cash rate" restrictive. Watch for a potential AUD rally if upcoming quarterly data confirms this domestic heat is persisting into the autumn months.

Join our FREE Macro Workshop at Global Markets Eruditio!

Is the RBA trapped by high energy costs? We’ll break down the Australian CPI vs. Fed Policy Divergence and show you how to trade the AUD/JPY as domestic inflation heats up.