U.S. Labor Market Holds Firm: Initial Jobless Claims Rise Slightly to 212,000

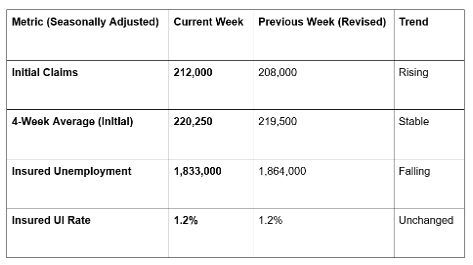

The U.S. labor market continues to exhibit remarkable resilience in the face of restrictive monetary policy. According to the Department of Labor’s report released on Thursday, February 26, 2026, seasonally adjusted initial unemployment claims rose to 212,000 for the week ending February 21.

While this represents a modest increase of 4,000 from the previous week’s revised level, the figure remains well within the range that economists associate with a healthy, stable job market. The data suggests that despite headlines of selective corporate restructuring in early 2026, broad-based layoffs have yet to materialize.

1. The Moving Averages: Filtering the Noise

To get a clearer picture of the labor trend, analysts look to the 4-week moving average, which strips out week-to-week volatility.

Initial Claims Average: The 4-week moving average edged up to 220,250, an increase of 750 from the prior week. This slight upward drift indicates a very gradual cooling of the labor market rather than a sharp correction.

Continuing Claims: For the week ending February 14, insured unemployment (those already receiving benefits) stood at 1,833,000, a decrease of 31,000. This suggests that while more people are applying for benefits, those already in the system are finding new roles at a steady pace.

2. Regional Hotspots and State-Level Shifts

The report highlighted significant geographical variations in the labor landscape.

Highest Unemployment Rates: For the week ending February 7, Rhode Island (3.0%), New Jersey (2.9%), and Massachusetts (2.7%) led the nation in insured unemployment rates.

Largest Decreases: Several major states saw a significant drop in new filings for the week ending February 14. New York recorded a massive decrease of 7,615 claims, followed by Pennsylvania (-5,201) and New Jersey (-2,845).

Minor Increases: Small upticks in claims were noted in Iowa (+377) and Michigan (+105), largely attributed to seasonal factors in the manufacturing and agricultural sectors.

3. Special Programs and Unadjusted Data

The unadjusted data showed an even more pronounced seasonal dip. Actual initial claims under state programs totaled 193,107, an 8% drop from the previous week.

Veterans and Federal Employees: Claims from newly discharged veterans decreased slightly to 428, while claims from former Federal civilian employees fell to 554.

Extended Benefits: No states triggered the "Extended Benefits" program, a clear sign that long-term unemployment remains near historical lows.

GME Academy Analysis: "The Fed’s Golden Path"

At Global Markets Eruditio, we analyze these claims as a key indicator for Federal Reserve policy.

Trader's Takeaway for February 2026:

USD Impact: These numbers are "just right" for the Greenback. They aren't high enough to spark recession fears, but they aren't low enough to suggest an overheating labor market that would force the Fed to hike rates again. This supports a neutral-to-bullish outlook for the USD.

Equities Sentiment: The drop in insured unemployment to 1.83 million is a positive sign for consumer-facing stocks. It shows that the "rehiring" process in the U.S. remains efficient, supporting household income and spending.

Yield Curve: We expect the 10-year Treasury yield to remain range-bound. As long as initial claims stay below the 250,000 threshold, the "soft landing" remains the base-case scenario for the U.S. economy.

Join our FREE Macro Workshop at Global Markets Eruditio!

Is the U.S. labor market finally cooling? We’ll analyze Initial Claims vs. Non-Farm Payrolls and show you how to trade the EUR/USD during the next jobs report.