Kiwi Spending Rebounds: NZ Retail Sales Defy Economic Chill in Q4 2025

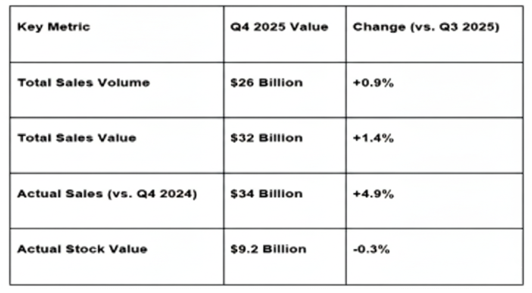

New Zealand’s retail sector showed unexpected resilience in the final months of 2025, with consumers opening their wallets despite a year marked by high interest rates and cautious sentiment. According to the December 2025 Quarter Retail Trade Survey released by Stats NZ, the total volume of retail sales rose 0.9 percent, signaling a steadying of the "nascent recovery" recently highlighted by RBNZ Governor Anna Breman.

Total seasonally adjusted sales reached $26 billion in volume and $32 billion in value, as 12 of the 16 regions across Aotearoa reported growth in spending.

1. Sector Winners: Health, Tech, and Travel

The growth was broad-based, with 12 out of 15 industries seeing higher sales volumes. The data suggests that New Zealanders prioritized health and home improvements while taking advantage of a booming tourism season.

Pharmaceutical & Health: This sector was the star performer, with sales volumes jumping 5.2 percent.

Hardware & Building: Signaling a potential bottoming out of the construction slump, hardware and garden supplies rose 2.2 percent.

The Tourism Boost: Accommodation values surged 5.1 percent ($71 million), likely driven by the record-high number of international visitors and domestic travelers during the Christmas period.

The "Looming" Lull: Conversely, motor vehicle and parts retailing saw a 1.7 percent drop in volume, reflecting continued consumer hesitation toward big-ticket "discretionary" purchases.

2. Regional Performance: Canterbury Leads the Charge

While Auckland provided the largest raw dollar increase, the Canterbury and Hawke’s Bay regions showed the strongest percentage growth, reinforcing Governor Breman’s recent comments in Christchurch regarding the region’s economic "bright spot" status.

Canterbury: Saw a robust 3.1 percent ($128 million) increase in sales value.

Auckland: Grew by 1.8 percent, contributing a massive $215 million to the national total.

Hawke’s Bay: Posted the highest regional percentage gain at 3.2 percent, showing a strong recovery in consumer confidence.

3. Inventory Management: Leaner Stocks for 2026

Retailers appear to be managing their back-of-house operations more tightly. The total value of actual stock held as of December 31, 2025, was $9.2 billion, down 0.3 percent from the previous year.

Clothing & Accessories: Stocks fell by 4.9 percent ($39 million), suggesting that retailers successfully cleared summer lines.

Furniture & Housewares: In contrast, stock values here jumped 11 percent ($39 million), potentially in anticipation of the projected housing market recovery in early 2026.

GME Academy Analysis: "The Consumer Resilience Play"

At Global Markets Eruditio, we believe these retail figures provide a crucial "second look" at the RBNZ’s recent decision to hold the OCR at 2.25%.

Trader's Takeaway for February 2026:

NZD Support: The 0.9% volume growth is slightly higher than market expectations. This provides a "fundamental floor" for the NZD, suggesting the economy isn't cooling as fast as some bears predicted.

Rate Outlook: Robust retail spending, particularly in services like accommodation and dining, might make the RBNZ cautious about cutting rates too early in 2026. If spending remains "hot," inflation in non-tradables could remain stubborn.

Equities: Watch for strength in listed retailers and tourism-adjacent stocks (like Air New Zealand and Auckland Airport) as the $34 billion actual spend figure highlights a strong "spending season."

Join our FREE Macro Workshop at Global Markets Eruditio!

Is the Kiwi consumer "tapped out" or just getting started? We’ll break down the NZ Q4 Retail Survey vs. Q1 2026 Forecasts and show you how to trade the NZD "Growth Divergence."