Growth at a Crawl: U.S. Business Activity Hits 10-Month Low Amid "Triple Threat"

The U.S. economic engine showed signs of significant overheating and subsequent stalling in February 2026. According to the latest S&P Global Flash PMI data released on February 20, private sector growth slowed to its weakest pace since April 2025. A "triple threat" of weakened demand, persistent price hikes, and severe winter weather has left the economy teetering on the edge of a mid-quarter slump.

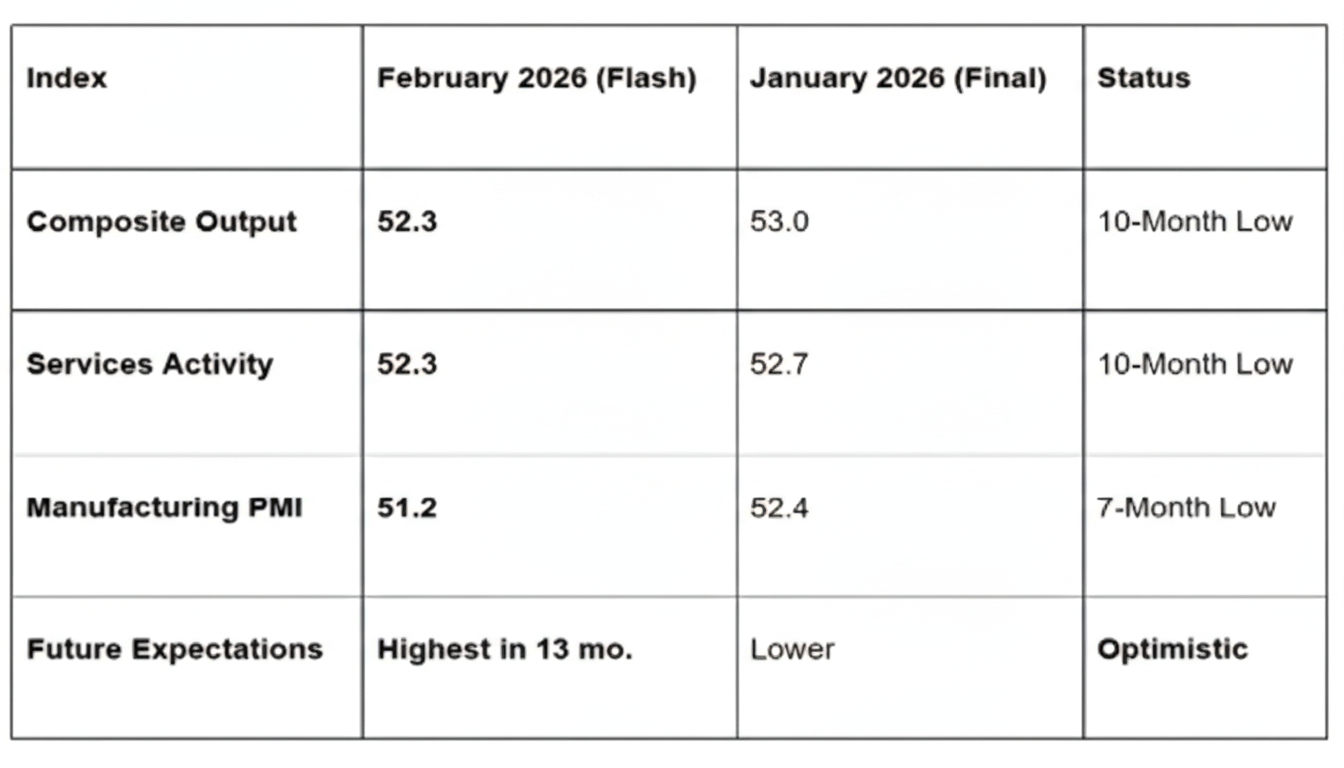

The Flash US Composite PMI Output Index fell to 52.3 in February, down from 53.0 in January. While any reading above 50.0 indicates expansion, the ten-month low suggests that the robust recovery seen in the latter half of 2025 is rapidly losing steam.

1. The Sector Breakdown: Services and Factories Cooling

The slowdown was broad-based, affecting both the service-providing and goods-producing sectors of the economy.

Services (10-Month Low): The Services PMI Business Activity Index dipped to 52.3. Service providers noted that while work inflows continued, the "chill" from high interest rates and stretched consumer affordability is finally setting in.

Manufacturing (7-Month Low): The Manufacturing Output Index mirrored the services score at 52.3, while the overall Manufacturing PMI slumped to 51.2. Factories reported a slight drop in new orders for the second time in three months, pointing to a genuine softening in industrial demand.

2. Costs and Tariffs: The Inflationary "Sting"

One of the most concerning aspects of the February report was the resurgence of price pressures. Average selling prices for goods and services rose at the steepest rate since last August.

The Tariff Trap: Chief Business Economist Chris Williamson noted that supplier price hikes are being heavily influenced by new tariff policies. These costs are being passed directly to consumers, with services inflation hitting a seven-month high.

Supply Chain Stutter: Supplier lead times lengthened to a degree not seen since the height of the pandemic (October 2022). While "bad weather" was a factor, businesses cited port congestion and tariff-related delays as the primary culprits behind dwindling input inventories.

Labor Market Freeze: Hiring has slowed to a "crawl." Payrolls rose only marginally for the third month in a row, as firms remain hesitant to expand headcounts in the face of rising wage demands and uncertain sales.

3. Looking Ahead: Is the Slump Temporary?

Despite the grim headline figures, American business leaders haven't lost hope.

Optimism Jump: Business expectations for the year ahead surged to a 13-month high.

The "Weather Rebound": Many firms believe that once the "extreme cold" of February passes, a wave of pent-up demand will return.

Policy Support: Survey respondents expressed confidence that government tax breaks and a potentially more stable interest rate environment later in 2026 will provide the necessary tailwinds for a spring recovery.

GME Academy Analysis: "The PMI-GDP Divergence"

At Global Markets Eruditio, we caution traders not to ignore the "stagflationary" signals in this data.

Trader's Takeaway for February 2026:

GDP Warning: Historically, a PMI of 52.3 is consistent with annualized GDP growth of approximately 1.5%. This aligns perfectly with the weak 1.4% Q4 GDP print, confirming that the "Shutdown Slump" has bled into the new year.

Currency Impact (USD): The combination of slowing growth and rising inflation (selling prices) puts the Fed in a corner. The US Dollar Index (DXY) may see short-term weakness if markets interpret this as a reason for the Fed to reconsider its "less accommodative" stance.

Sector Focus: We remain Underweight Manufacturing as export orders continue to slide. We are Neutral on Services, watching for a weather-driven rebound in March.

Join our FREE Macro Workshop at Global Markets Eruditio!

Are we headed for a "Soft Landing" or a "Hard Stall"? We’ll analyze the S&P Global Final PMI Revisions and show you how to trade the "Weather vs. Tariffs" narrative.