Signal or Noise? Fed Governor Waller Questions "Stale" January Jobs Data

In a high-stakes address at the National Association for Business Economics (NABE) on February 23, 2026, Federal Reserve Governor Christopher J. Waller provided a candid roadmap for the FOMC’s March meeting. Waller, who famously dissented against the January decision to hold rates steady, argued that while recent data suggests a turnaround, the U.S. labor market remains "weak and fragile" following the lackluster performance of 2025.

Waller’s speech, titled "Labor Market Data: Signal or Noise?", highlighted the deep uncertainty currently paralyzing central bank policy as they navigate the aftermath of last year’s government shutdown and the volatility of "Tariff-Push" inflation.

1. The Dissent: Why Waller Wanted a January Cut

Waller revealed the rationale behind his rare dissent at the January 2026 meeting, where he favored a 25-basis-point cut while his colleagues opted to pause.

The 2025 "Black Hole": Waller noted that 2025 was the weakest year for job creation since 2002 (outside of a recession). Revised data suggests payroll employment likely fell in 2025—the first time this has happened unrelated to a recession since 1945.

Underlying Inflation: While headline PCE is near 3%, Waller argues that "underlying inflation" (stripping out temporary tariff effects) is already close to the 2.0% goal.

Risk Management: For Waller, the risk of a "substantial downturn" in the labor market outweighed the risk of an inflation flare-up, justifying a move toward a neutral rate sooner rather than later.

2. January’s Surprise: Signal or Statistical Noise?

The January employment report showed a massive 130,000 job gain, far exceeding expectations. However, Waller remains skeptical, citing several "asterisks" that could see these numbers revised away:

Sector Concentration: Nearly the entire gain (125,000 out of 130,000) came from healthcare and social assistance.

Conflicting Private Data: While the government reported 172k private-sector gains, ADP reported only 22k, and Revelio estimated a mere 3k.

The "Wealth Gap" Spending: Waller warned that resilient GDP (1.4% in Q4 2025) is being driven by the top 20% of "stock-rich" households, masking a "pinch" felt by the bottom 60% of earners who account for nearly half of all spending.

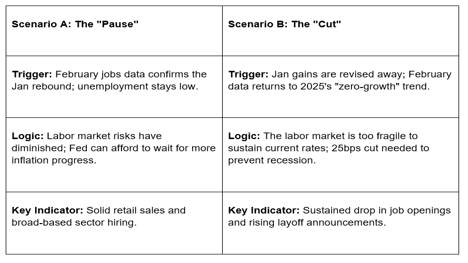

3. The March 17-18 "Coin Flip"

Waller essentially categorized the upcoming March FOMC decision as a 50/50 toss-up, depending entirely on the data arriving over the next three weeks.

4. The Supreme Court "Tariff" Wildcard

Waller addressed the Supreme Court ruling from last Friday, which overturned a large share of import tariffs. While markets expect this to be disinflationary, Waller remained cautious:

Administration Response: Uncertainty remains high as the Trump Administration seeks to reimpose tariffs under different legal authorities.

"Look Through" Policy: Waller emphasized that just as he "looked through" tariff-driven price spikes on the way up, he will ignore their removal on the way down, focusing instead on core inflationary trends.

GME Academy Analysis: "The Waller Pivot"

At Global Markets Eruditio, we see Waller’s speech as a crucial "reality check" for USD bulls who were betting on a hawkish Fed pivot.

Trader's Takeaway for February 2026:

USD Sensitivity: The DXY will likely be extremely sensitive to the March 6 Employment Report. If that report is weak, Waller’s "cut" scenario becomes the base case, potentially weakening the Dollar.

Yield Curve: We expect the front end of the curve (2-year Treasury) to remain volatile as it prices and de-prices that 25bps March cut.

Consumer Staples: Waller’s comments on the "squeezed" lower 60% of households suggest a cautious outlook for discretionary retail stocks compared to discount-oriented staples.

Join our FREE Macro Workshop at Global Markets Eruditio!

Will the Fed cut in March? We’ll analyze the Feb 27 Producer Price data and the March 6 Jobs Report in real-time to find the Waller "Signal."