The $100 Trillion Shadow: Global Debt and Currency Crisis Risks

As we navigate February 2026, the global financial landscape is defined by a staggering paradox: while GDP growth remains resilient at 3.3%, global public debt is hurtling toward the $100 trillion mark. IMF Managing Director Kristalina Georgieva recently warned at Davos that this debt is a "very heavy burden" approaching 100% of global GDP, creating a fragile environment where even minor market tremors could trigger a full-scale currency crisis.

At the GME Academy, we monitor these "debt-to-GDP" ratios as the ultimate barometer of national solvency. When debt becomes unsustainable, the first casualty is almost always the domestic currency.

1. The Advanced Economy Strain: A "Widow-Maker" Return

For the first time since the Napoleonic Wars, advanced economies are seeing debt levels exceed 110% of GDP.

The US Deficit: Despite robust growth, the US deficit remains high at 5.5%, pushing total debt past $36 trillion (123% of GDP). This "fiscal dominance" limits the Federal Reserve's ability to fight future inflation without risking a government default.

Japan’s Yield Surge: The "widow-maker" trade—betting against Japanese bonds—has finally paid off. In early 2026, 10-year yields surged past 2%, and the Yen saw violent swings as authorities intervened to prevent a total currency collapse.

The "K-Shaped" Risk: Wealth inequality in developed markets is creating political pressure for even more government spending, further bloating balance sheets.

2. Emerging Markets: Resilience vs. The "Sudden Stop"

Ironically, many Emerging Markets (EMs) enter 2026 with healthier fiscal balance sheets than their developed counterparts. Most EMs average debt levels below 60% of GDP.

The Philippines Case: While the Philippine debt-to-GDP ratio is projected to hit a 20-year high of 65.7% by the end of 2026, analysts argue the trajectory is manageable because much of it was used to lock in low-interest "cash buffers" during the pandemic.

The "Sudden Stop" Risk: Despite better fundamentals, EMs are vulnerable to "contagion." If US yields spike due to debt concerns, capital can flee EMs in a "sudden stop," causing local currencies like the PHP or IDR to crash regardless of their domestic health.

3. The Anatomy of a 2026 Currency Crisis

How does a debt problem turn into a currency crisis? The process follows a predictable, high-speed chain reaction:

Confidence Shock: Investors begin to doubt a government’s ability to service its debt.

Yield Spike: Investors demand higher interest rates to hold the "risky" debt.

Monetization Fear: Markets fear the central bank will print money to pay the debt (inflationary).

Capital Flight: Both domestic and foreign investors dump the currency to buy Gold or USD.

The "Death Spiral": As the currency weakens, the cost of servicing foreign-denominated debt rises, making the debt even more unsustainable.

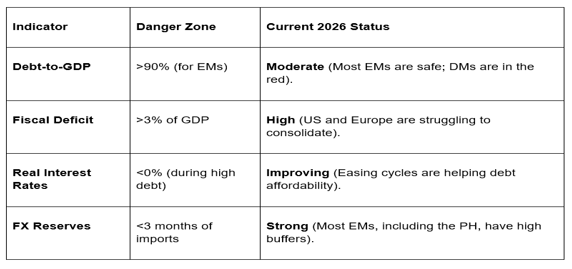

4. Key Indicators to Watch (The Red Flags)

The GME Academy Analysis: "Hedging the Debt Bomb"

At Global Markets Eruditio, we believe 2026 is the year of "Currency Differentiation." Markets are no longer treating all Emerging Markets as "risky" and all Developed Markets as "safe."

Trader's Takeaway:

Watch the Bond Vigilantes: If you see yields on long-term government bonds rising faster than short-term rates (steepening curve), it’s a sign the market is "revolting" against debt levels.

Gold as the "Anti-Debt" Asset: Gold’s rise to $5,000+ in 2026 is the ultimate proof that investors are losing faith in fiat debt. It should be a staple in any "crisis" portfolio.

PHP Strategy: Keep a close eye on the ₱60:$1 mark. While the BSP has reserves, a global "flight to quality" triggered by a US or European debt scare would override domestic fundamentals.

Join our FREE Forex Workshop at Global Markets Eruditio!

Is your portfolio protected against a sovereign default? We’ll show you how to use Credit Default Swaps (CDS) as a leading indicator for currency moves and how to hedge your savings against "imported" inflation.